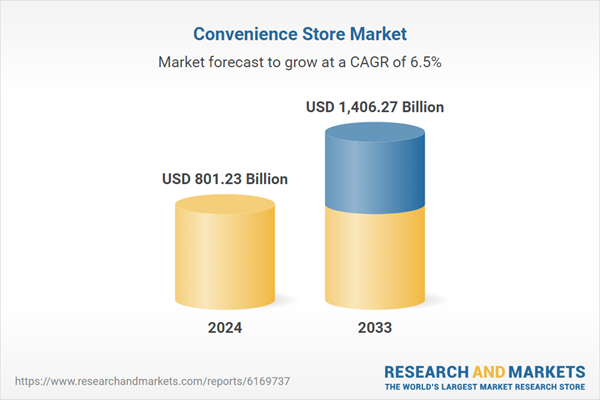

The Convenience Store Market is on track for substantial growth, expected to increase from USD 801.23 billion in 2024 to USD 1.40 trillion by 2033. This significant rise reflects a growing consumer preference for quick and easy shopping options, driven by fast-paced lifestyles and a demand for grab-and-go products. The market is projected to achieve a compound annual growth rate (CAGR) of 6.45% from 2025 to 2033, suggesting a wave of new opportunities and innovations in the retail sector.

The growth of the convenience store market can be attributed to increasing urbanization and the evolving lifestyles of consumers. With longer working hours and busier schedules, shoppers are looking for nearby stores that provide quick access to groceries, snacks, and essential items. Convenience stores meet this demand by offering immediate purchase options without the extensive checkout lines typical of larger supermarkets. Furthermore, their extended operating hours, which often include 24/7 service in certain areas, boost accessibility for urban dwellers. Currently, more than half of the global population, approximately 56.2 percent, lives in urban settings, particularly in regions like Latin America and the Caribbean, where urbanization rates exceed 80 percent. The United Nations projects that this trend will continue, with 68 percent of the global population expected to reside in urban areas by 2050.

Another factor contributing to the popularity of convenience stores is their evolving product offerings, particularly the introduction of ready-to-eat meals, fresh produce, and healthier snack options. The shift toward on-the-go consumption has led to increased sales of items such as fresh sandwiches, meal kits, salads, and beverages. Retailers are responding to consumer preferences by providing more health-conscious and premium products. This expansion of food categories positions convenience stores as strong competitors to both quick-service restaurants and traditional supermarkets.

Technological advancements also play a significant role in the convenience store sector”s growth. The integration of digital payment systems, self-checkout kiosks, and loyalty mobile applications is enhancing both shopping efficiency and customer experience. Many retailers have adopted mobile ordering, curbside pickup, and delivery services, particularly in response to changing consumer habits following the COVID-19 pandemic. Additionally, data analytics enable retailers to personalize promotions and optimize inventory management, appealing to tech-savvy consumers while streamlining operations.

However, the convenience store market faces intense competition from supermarkets, hypermarkets, and online grocery platforms that offer a broader range of products at lower prices. Traditional retailers benefit from economies of scale, allowing them to set prices that smaller convenience outlets cannot match. E-commerce giants also provide home delivery services that entice customers away from physical stores. To remain competitive, convenience stores must differentiate themselves by emphasizing location convenience, personalized service, and specialized product selections.

Furthermore, operational challenges are prevalent in the convenience store sector, particularly high expenses related to rent, utilities, and labor costs in urban centers. Supply chain disruptions—exacerbated by global events—further complicate product availability and pricing. Smaller convenience store operators often lack the bargaining power of larger retailers, leading to higher procurement costs and reduced profit margins. Balancing stable inventory levels and competitive pricing while maintaining profitability presents a significant challenge. Without strategic partnerships and effective logistics, convenience stores risk losing ground to more dominant retail players.

For more detailed insights, the “Convenience Store Market Report by Type, Product, Distribution Channel, Countries and Company Analysis, 2025-2033” is available through ResearchAndMarkets.com.