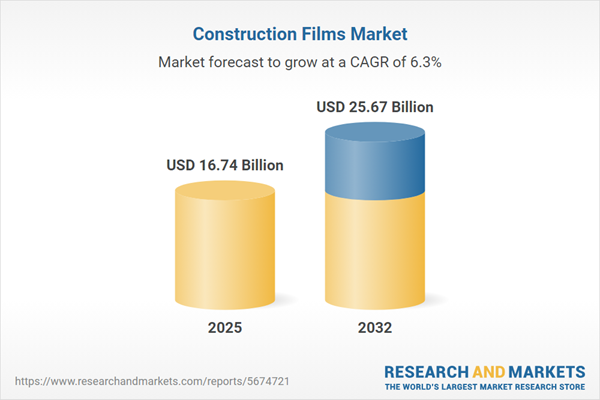

The global market for construction films is poised for significant expansion, driven by advancements in eco-friendly technologies, smart innovations, and stringent sustainability regulations. A recent report from ResearchAndMarkets.com highlights that the market, valued at USD 15.76 billion in 2024, is anticipated to grow to USD 16.74 billion in 2025, with a compound annual growth rate (CAGR) of 6.29%, ultimately reaching USD 25.67 billion by 2032.

This comprehensive analysis of the construction films sector emphasizes critical insights into emerging trends and essential strategies for industry players. In recent years, construction films have become integral to modern architectural design, merging innovative practices with environmental standards and evolving end-user needs.

Advancements in polymer formulations have significantly improved the durability, UV resistance, and moisture control features of construction films, making them suitable for a wide range of applications, from underlayments to decorative surfaces. These enhancements are crucial for industry decision-makers aiming to comply with rigorous standards and embrace eco-friendly technologies that contribute to circular economy initiatives.

The report identifies transformative factors reshaping the construction films industry”s value chain. Sustainability has shifted focus towards bio-based polymers and recycled materials, while digitalization, driven by Industry 4.0 principles, enhances efficiency and minimizes waste. Innovative products, such as nanocomposite films and advanced fire-retardant additives, broaden application potential, illustrating the intersection of sustainability, technology, and material innovation.

In 2025, the United States implemented tariffs on essential polymer imports, which have markedly impacted the global construction films supply chain. These tariff adjustments have raised raw material costs, compelling manufacturers to reassess their sourcing strategies and seek alternative procurement avenues. Consequently, this has led to increased logistical complexities and fostered innovation in sourcing and supply chain management, highlighting the necessity for transparent cost frameworks and strategic adjustments.

The report further outlines market segmentation by product types, applications, end users, thickness levels, and distribution channels. Key insights include:

- Product Types: High-performance polyethylene (HDPE, LDPE, LLDPE), polypropylene (BOPP, Cast PP), and various PVC types drive usage across multiple applications.

- Applications: Films serve diverse needs in interior decoration, roofing, and waterproofing, with demand spread across commercial, industrial, and residential sectors.

- End Users: The market is divided among commercial, industrial, and residential users, each with distinct requirements and applications.

- Thickness Levels: Different thicknesses cater to various protective and structural needs.

- Distribution Channels: Customized engagement strategies are essential for navigating direct sales, distributor networks, and online platforms.

The report also highlights regional dynamics within the construction films market. In the Americas, infrastructure investments and sustainability regulations are driving demand, while in the EMEA region, environmental mandates and renovation activities are propelling the growth of high-performance films that comply with fire safety standards. Meanwhile, rapid urbanization in the Asia-Pacific region is increasing the need for energy-efficient solutions, with an uptick in the adoption of solar and waterproofing films.

Ultimately, the construction films market is expected to thrive, fueled by sustainability initiatives and innovations in advanced materials. The impact of U.S. tariffs underscores the need for strategic sourcing and diversification in supply chains, while grasping regional market dynamics will enable tailored market entry and operational strategies.