The complement 3 glomerulopathy market is anticipating remarkable growth, with a compound annual growth rate (CAGR) of 37.2% projected from 2025 to 2034. This acceleration is attributed to the introduction of innovative therapies targeting complement components such as C3, C5, MASP-3, and RNA interference (RNAi).

According to a recent report by DelveInsight, the increasing awareness of the disease, advancements in research related to the complement pathway, and improved diagnostic rates are key factors propelling market expansion. The absence of approved targeted therapies has led to significant investments in research and development for complement inhibitors and novel biologics.

Pipeline therapies like KP104 from Kira Pharmaceuticals, Zaltenibart from Omeros Corporation, Ruxoprubart from NovelMed Therapeutics, and ARO-C3 from Arrowhead Pharmaceuticals are anticipated to transform the treatment landscape for complement 3 glomerulopathy over the next decade.

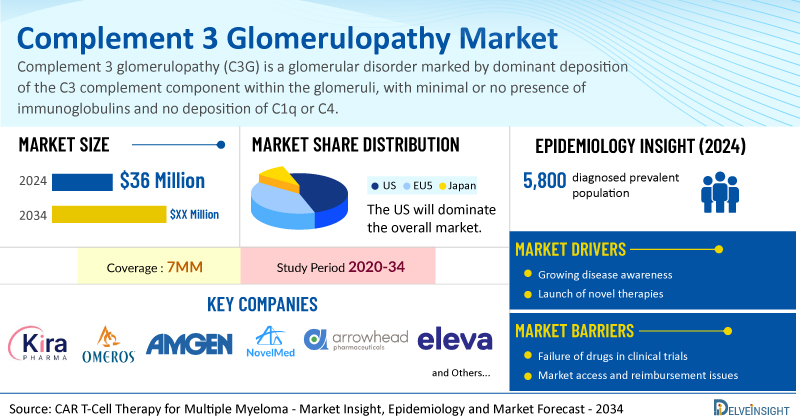

In 2024, the overall market size for complement 3 glomerulopathy was estimated at USD 36 million across major markets. The United States represented the largest segment, accounting for roughly 73% of the total market share among seven major markets (7MM), which also include the EU4 countries (Germany, France, Italy, and Spain), the United Kingdom, and Japan.

The diagnosed population of patients with complement 3 glomerulopathy in the 7MM was around 5,800 in 2024. This figure is expected to rise through 2034, driven by advancements in complement biology, enhanced diagnostics, and broader applications of genetic testing, complement assays, and multidisciplinary biopsy evaluations.

Key players in the complement 3 glomerulopathy space, including Kira Pharmaceuticals, Omeros Corporation, Amgen, NovelMed Therapeutics, Arrowhead Pharmaceuticals, and Eleva, are actively developing innovative drugs for this condition. Noteworthy therapies in clinical trials include KP104, Zaltenibart (OMS906), TAVNEOS (avacopan), Ruxoprubart (NM8074), and ARO-C3.

The urgent need for effective treatments is highlighted by the current reliance on off-label medications, which underscores the significant unmet need for approved therapies. Current treatment strategies primarily utilize immunosuppressants, corticosteroids, and various supportive agents, emphasizing the importance of new targeted therapies that can address the underlying causes of the disease.

Recent developments include the FDA”s approval of pegcetacoplan for the treatment of complement 3 glomerulopathy and related conditions in patients aged 12 years and older. Additionally, Novartis has received positive opinions from the EMA for its drug, iptacopan, indicating a shift towards more effective treatment options in the near future.

As the complement 3 glomerulopathy market continues to evolve with these promising therapies, it is expected to set new standards of care and drive both innovation and economic growth in the healthcare sector.